Understanding Your KiwiSaver

Started in July 2007, KiwiSaver is a voluntary retirement savings scheme to help you save for your future. Available for all New Zealand citizens and permanent residents living in NZ, it is run by independent providers who you choose to manage your savings. These providers invest their members’ KiwiSaver funds to make a greater return on the savings for their retirement.

Joining

When you start a new job, your employer will automatically enrol you in KiwiSaver if you’re eligible and:

- you’re between the ages of 18 and 65

- your job is full time or permanent part-time

- you’re on a contract of more than 28 days

- you’re a casual agricultural worker for more than 3 months.

If you do not get automatically enrolled, you can join by asking your employer, or directly with a KiwiSaver provider. Your employer should give you a KiwiSaver information pack KS3.

You have 8 weeks to see if you want to be in KiwiSaver or not. If you do not want to be in KiwiSaver, you can opt-out.

Choosing a Scheme Provider

It’s important that you choose a KiwiSaver provider that you trust and are comfortable with, after all, they are going to be in control of your money. If you are auto-enrolled into KiwiSaver and do not choose a prover yourself, the IRD will allocate one to you from their default list. If you want to have a more active role in choosing who is in control of your money, then we suggest you contact a KiwiSaver specialist or one of our team to help guide you through the process.

What fund is right for you?

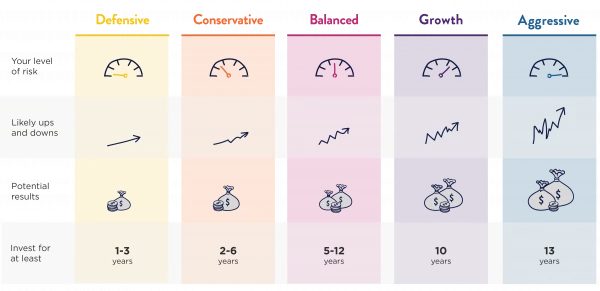

Choosing the right fund is as important as choosing the right provider. Your provider may offer a range of different investment funds to suit your needs. These funds will come with varying amounts of potential risk and return. We all know the adage ‘greater risk equals greater return’. Sorted.org.nz have created a great chart (shown below) that breaks down the many KiwiSaver funds into five groups. Their fund finder and Smart Investor platform can help you compare KiwiSaver funds and pick one that is right for you. And don’t forget, once in KiwiSaver you can change your chosen fund at any time.

It’s important to note that KiwiSaver investments are not guaranteed by the Government. So it’s crucial that you make informed decisions about your money and understand the varying amounts of risk.

Contributions

The minimum rate you can contribute (called your deductions) to your KiwiSaver fund is 3% of your before-tax pay, but if you want to contribute more you can choose 4%, 6%, 8%, or 10%. If you do not choose a rate your employer will deduct 3%. Deductions begin from your first pay.

Your employer must also make compulsory contributions of at least 3% of your gross earnings on top of your regular pay. In essence, if you choose to contribute 3%, then your employer is matching that contribution. Some employers will offer a higher contribution than 3% but this isn’t mandatory and would be something negotiated in each individual’s employment contract.

Free money

There is a yearly government contribution to KiwiSaver members who have contributed a minimum of $1,042.86 by the end of June. This contribution is a whopping $521.43, or $0.50 per dollar of the minimum contribution. It’s a good idea to log onto your KiwiSaver account and make sure that you have contributed enough each year. You don’t want to miss out on free money!

As with any decisions surrounding finances, it can all be a little overwhelming. If you would like to talk to someone about your situation and get help building a new financial plan, then get in touch with the team here at Accountants Plus. We have years of experience in the financial world and can provide practical individual and business advice tailored to your needs. Contact us today.